Indemnification Clauses Explained & How to Negotiate Them in 2026

Learn what indemnification clauses actually mean for your small business, plus practical negotiation tactics to limit your liability and protect cash flow.

Indemnification Clauses Explained & How to Negotiate Them in 2026

If you run a small business, you’ve probably skimmed past indemnification clauses and assumed they were standard legal boilerplate. In reality, this single section often determines whether a lawsuit against your vendor lands on your doorstep or stays where it belongs. Understanding how indemnity works—and knowing exactly where to push back—can save your company from catastrophic out-of-pocket losses.

What indemnification actually means

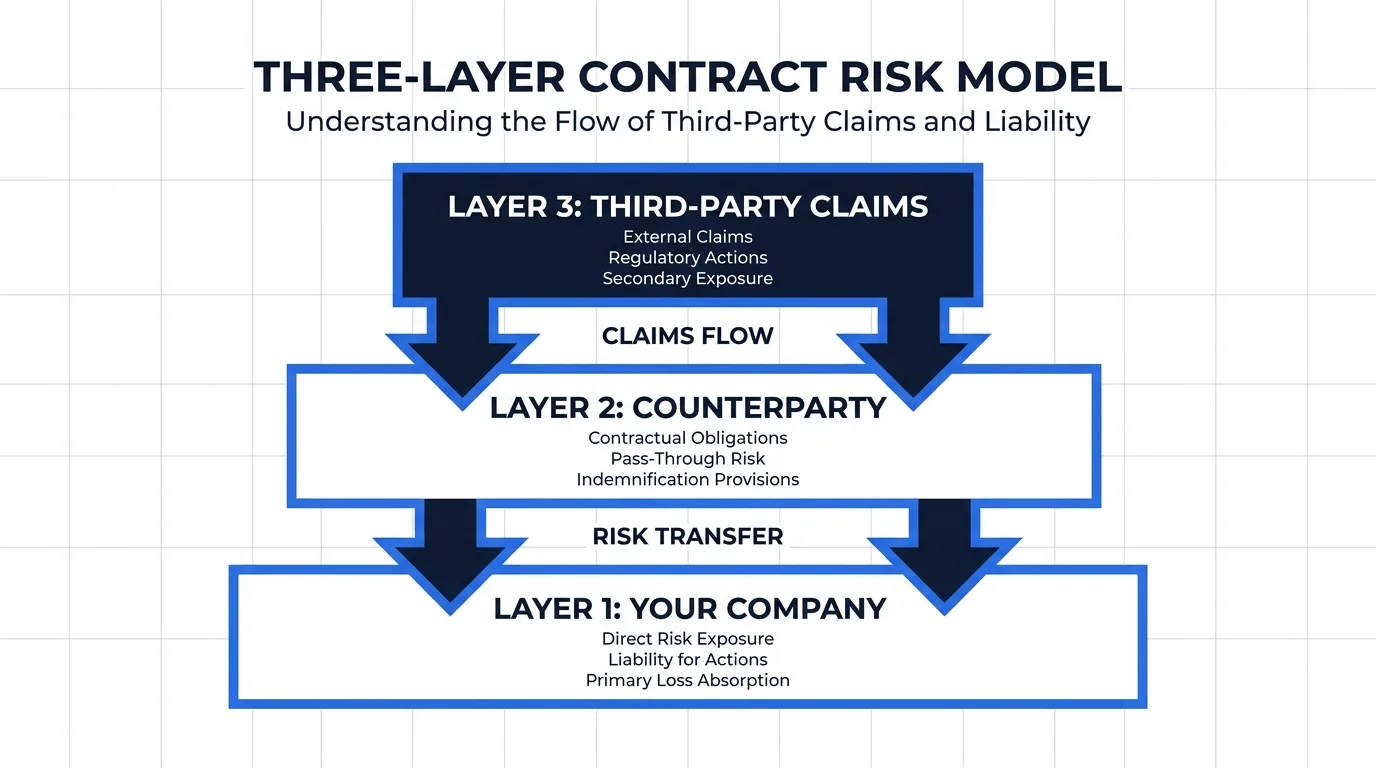

At its core, an indemnification clause is a risk-transfer mechanism. It states that one party agrees to compensate the other for specified losses, damages, or legal costs that arise from a covered event. In contract language, the protected party is the indemnified, and the party assuming the risk is the indemnitor.

Most small business owners focus on price and delivery timelines. But indemnification is where hidden liability hides. A poorly drafted clause can force you to cover legal fees, settlements, or regulatory fines that have nothing to do with your actual operations. Before you sign anything, treat this section like a financial audit, not a formality.

The three main types of indemnity clauses

Not all indemnification language is written the same way. Contracts typically fall into one of three structures:

- Unilateral indemnity: Only one party (usually the vendor or service provider) agrees to indemnify the other. This is common in SaaS agreements and vendor contracts.

- Mutual indemnity: Both parties agree to cover each other’s losses under similar conditions. Often seen in partnerships and joint ventures.

- Limited/specific indemnity: The clause only covers narrowly defined risks, such as intellectual property infringement or personal injury caused by negligence.

Knowing which type you are looking at sets the stage for negotiation. Mutual or limited clauses are generally friendlier to small businesses than broad unilateral language.

Red flags small businesses should never ignore

Some indemnification wording looks standard but quietly shifts unacceptable risk onto you. Watch for these patterns:

- Overbroad triggers: “Any and all claims, losses, or damages arising out of this agreement” without limiting the cause.

- Missing defense obligations: The clause requires you to pay but never mentions that the other party must handle the legal defense.

- No carve-outs: Fails to exclude indirect damages, consequential losses, or your own gross negligence.

- Uncapped exposure: Leaves you financially responsible for unlimited amounts, even if your contract value is $10,000.

- One-sided notice requirements: Forces you to notify them within 24 hours while giving them 30 days to respond.

If you spot more than two of these in a single contract, pause before signing. You can absolutely renegotiate these terms.

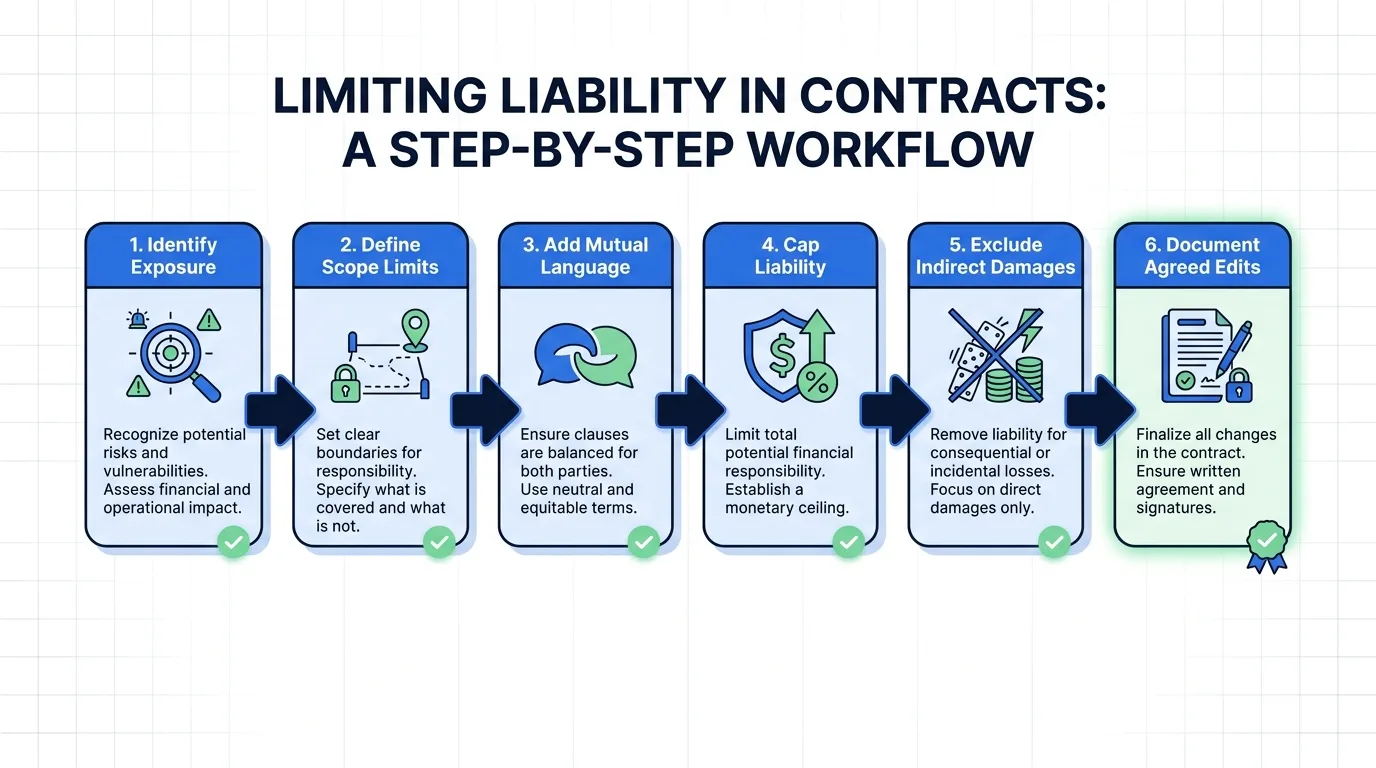

How to negotiate indemnification clauses

Negotiating indemnity isn’t about winning a legal battle—it’s about aligning risk with control. Here is a practical approach:

- Map your actual exposure. Ask yourself: what could realistically go wrong under this agreement? If you are a marketing agency, IP infringement is a real threat. If you are a logistics provider, third-party property damage is the concern.

- Push for mutual language. Even if you do not expect to invoke it, mutual indemnity creates balance and signals good faith.

- Add a defense obligation. Require the indemnitor to control the legal defense and cover all associated costs, not just the final settlement.

- Cap your liability. Tie the indemnification cap to the contract value or a fixed annual amount. Unlimited exposure is rarely acceptable for small businesses.

- Carve out exclusions. Explicitly exclude indirect damages, lost profits, and claims caused by your own willful misconduct or gross negligence.

- Align with your insurance. Verify that the indemnity aligns with your existing commercial general liability or professional indemnity insurance. Many policies will not cover contractual liability unless the clause specifically matches your policy wording.

When drafting edits, clarity beats legal jargon. Plain language reduces ambiguity and makes enforcement easier if a dispute ever arises. For a quick, jargon-free breakdown of your specific contract language, you can run it through an AiDocX AI review to see exactly how the indemnification clause reads in plain English before you respond.

Real-world examples: weak vs. balanced language

Comparing drafts makes negotiation easier. Here is how the same concept looks on opposite ends of the spectrum:

Weak (vendor-friendly): “Client agrees to indemnify, defend, and hold harmless Vendor from any and all claims, losses, damages, or expenses, including legal fees, arising out of or related to this Agreement, without limitation.”

Balanced (small-business friendly): “Each party agrees to indemnify, defend, and hold harmless the other party from third-party claims arising from its negligent acts or willful misconduct, breach of representation, or unauthorized use of the other party’s materials. This obligation does not cover indirect damages, lost profits, or claims caused by the indemnified party’s own gross negligence. Total liability under this section shall not exceed the total fees paid under this Agreement in the twelve months preceding the claim.”

Notice the differences: defined triggers, mutual language, excluded damages, and a clear cap. That is the standard you should aim for. Courts in most jurisdictions will enforce these clauses as written, but they also look for fairness and mutual assent. Drafting balanced language upfront removes that uncertainty.

Your pre-signoff indemnification checklist

Before you execute the contract, run through this list:

- Identify whether the clause is unilateral, mutual, or limited

- Verify that the indemnitor controls the legal defense

- Confirm a liability cap is included or negotiate one

- Check for exclusions covering indirect damages and gross negligence

- Ensure notice periods are reasonable and symmetric

- Cross-reference the indemnity cap with your insurance coverage

- Document any negotiated changes in the final executed copy

If any box stays unchecked, request a revision. Small adjustments now prevent expensive disputes later.

Final thoughts

Indemnification clauses are not obstacles—they are negotiation tools. The parties who understand them early consistently walk away with better risk alignment and stronger cash flow protection. Treat every contract review as a risk-mapping exercise, push back on overbroad language, and never sign unlimited exposure. Your business deserves clauses that protect it, not ones that quietly fund someone else’s mistakes.

Ready to automate your documents with AI?

Start free with AiDocX — AI contract drafting, meeting minutes, consultation notes, e-signatures, and more in one platform.

Get Started FreeMore from AiDocX Blog

Data Processing Agreement Template 2026: GDPR & PIPL Guide

Get the 2026 DPA template. Learn when you legally need one, required clauses for GDPR/PIPL compliance, and how to draft a robust contract for your clients.

Are E-Signatures Legally Binding in 2026? A Practical Guide

Discover if e-signatures are legally binding in 2026. Learn about ESIGN, eIDAS, and audit trails to ensure your digital contracts hold up in court.

NDA & Confidentiality Templates 2026: Types, Clauses, Sign

Master NDAs in 2026. Compare one-way vs mutual types, identify critical protective clauses, and learn how to e-sign contracts in minutes with AiDocX.