SAFE vs Convertible Note: Which Should Your Startup Use to Raise (2026)

A founder's plain-English comparison of SAFEs and convertible notes — how each works, valuation caps and discounts, interest and maturity, dilution, and when to choose one over the other for your early raise.

SAFE vs Convertible Note: Which Should Your Startup Use to Raise

When you raise your first money, you usually don't sell shares directly — pricing a company with no revenue is guesswork, and a priced round is slow and expensive. Instead, most early startups raise on an instrument that converts into equity later, at the next priced round. The two dominant choices are the SAFE and the convertible note. They look similar on the surface and produce a similar result — but the differences matter, and founders who blur them get surprised at conversion.

Here's the plain-English comparison.

What They Actually Are

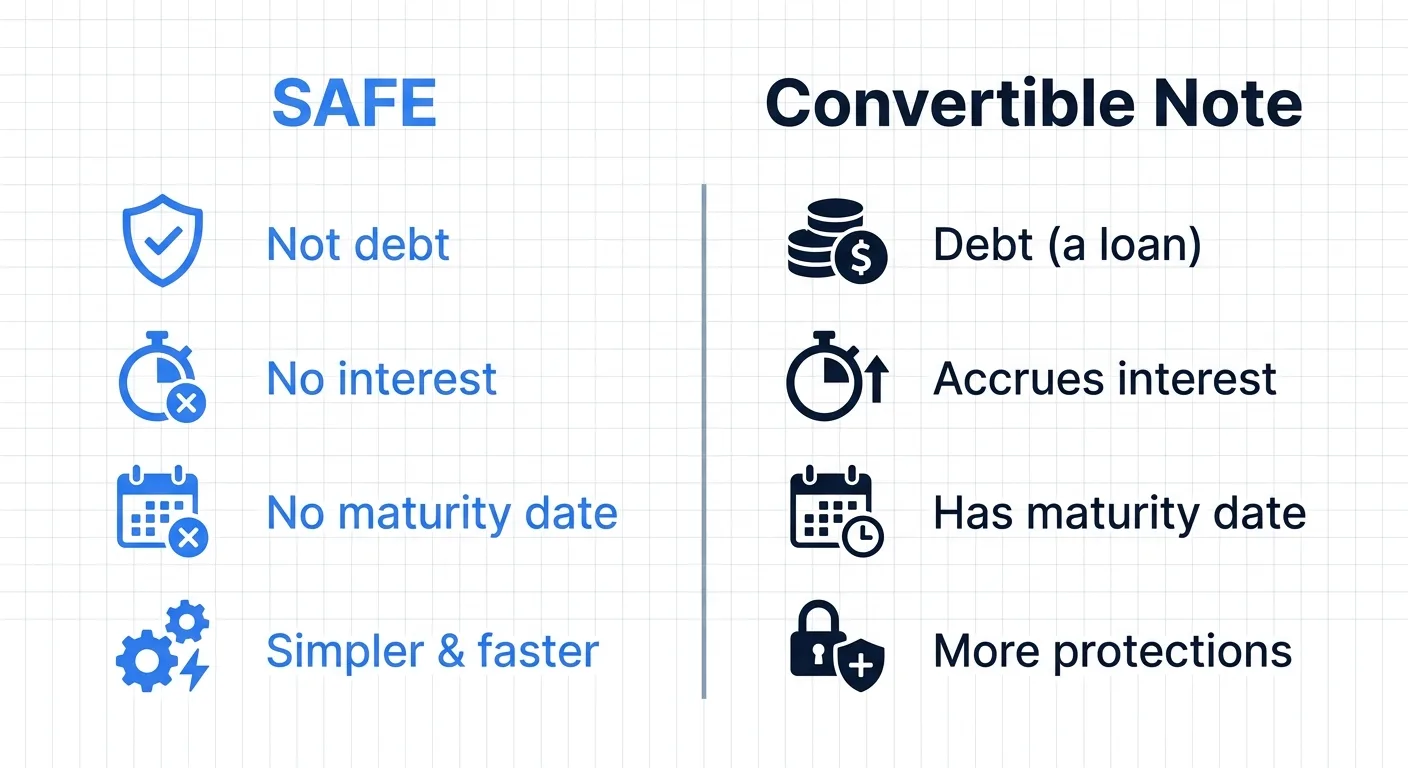

A convertible note is debt. The investor loans the company money. The loan accrues interest and has a maturity date. Instead of being repaid in cash, it's designed to convert into equity at a future financing — typically at a discount and/or a valuation cap.

A SAFE (Simple Agreement for Future Equity) is not debt. It's an agreement that gives the investor the right to equity in a future round. No interest, no maturity date, no repayment obligation. It was designed to strip a convertible note down to just the part everyone actually cared about — the future conversion — and remove the debt mechanics.

That single distinction — debt vs. not — drives almost every other difference.

The Terms That Decide the Outcome

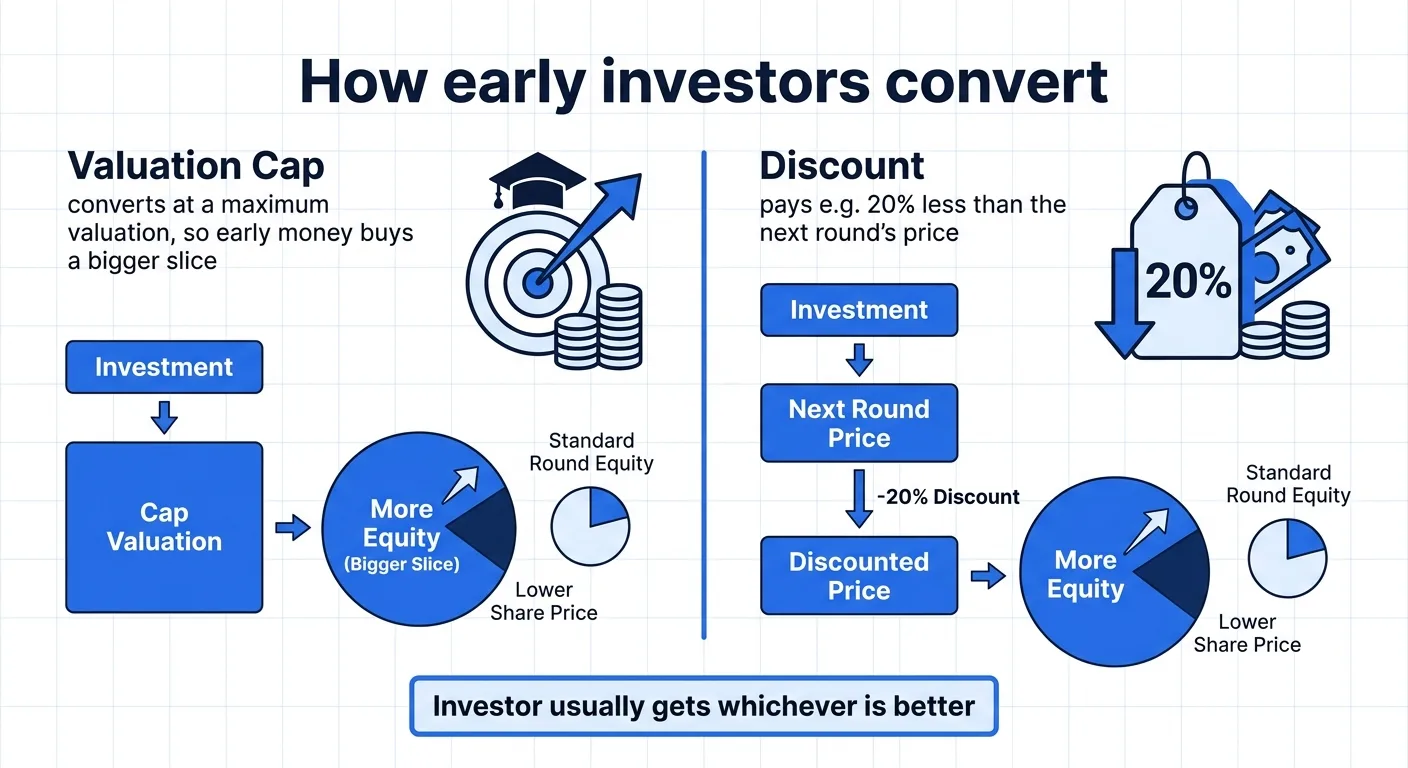

Both instruments usually share two key levers that determine how many shares the early investor gets when they convert:

- Valuation cap. The maximum company valuation at which the investment converts. A lower cap means the early investor's money buys a bigger slice — their reward for backing you first.

- Discount. A percentage discount (often 10–20%) on the price the next round's investors pay. Where both a cap and a discount exist, the investor typically gets whichever is better for them.

Convertible notes add two more that SAFEs drop:

- Interest rate. The note accrues interest (often a few percent), which increases the amount that converts into equity.

- Maturity date. A deadline (commonly 18–24 months) by which the note must convert or be repaid. If you haven't raised a qualifying round by then, you're technically in default territory and renegotiating — a real pressure point.

SAFE vs Convertible Note at a Glance

| SAFE | Convertible Note | |

|---|---|---|

| Legal nature | Not debt | Debt (a loan) |

| Interest | None | Yes, accrues |

| Maturity date | None | Yes (e.g. 18–24 months) |

| Repayment risk | None | Can come due if no round happens |

| Complexity | Simpler, faster, cheaper | More terms to negotiate |

| Investor protection | Lower (no debt claim) | Higher (creditor + interest) |

| Common with | Standardized seed rounds | Investors wanting debt protections |

When to Use Which

Lean toward a SAFE when you want to move fast and cheap, you're raising from investors familiar with the standard documents, and you'd rather not have a maturity-date clock ticking. For many early-stage startups today, a standardized SAFE is the default — minimal negotiation, low legal cost, founder-friendly.

Lean toward a convertible note when an investor specifically wants the protections of debt — interest and a maturity date — or when your local market and investors are simply more comfortable with notes than with SAFEs. In some regions, notes remain the norm and SAFEs are still unfamiliar to local counsel.

There's no universally "correct" answer; it depends on your investors, your market, and how much leverage you have. What's not optional is understanding the cap, discount, and (for notes) the maturity before you sign.

The Dilution Trap Founders Miss

Because SAFEs and notes convert later, it's easy to lose track of how much of the company you've actually promised away. Each instrument stacks: raise on three SAFEs with different caps, and at the priced round they all convert at once, sometimes diluting founders more than expected — especially when a low cap meets a much higher round price.

Before you sign each instrument, model the conversion on a fully-diluted basis. The number that matters is not how much cash you're raising today, but how much of the company you'll own after everything converts at the next round. Founders who track this in a running cap table avoid the unpleasant surprise; those who don't, discover it at the worst possible moment.

Frequently Asked Questions

Is a SAFE better than a convertible note? Neither is universally better. A SAFE is simpler, faster, and cheaper, with no interest or maturity date. A convertible note gives investors debt protections (interest and a deadline). The right choice depends on your investors and market.

Does a SAFE have a maturity date? No. Unlike a convertible note, a SAFE has no maturity date and no interest — it simply converts into equity at a future qualifying round. That's the main reason founders find SAFEs less stressful.

What is a valuation cap on a SAFE or note? A valuation cap is the maximum company valuation at which the investment converts into shares. A lower cap means the early investor's money converts into a larger ownership stake — compensation for investing early and taking more risk.

Do SAFEs and convertible notes dilute founders? Yes — both convert into equity at your next priced round, diluting existing shareholders. Because conversion is deferred, the dilution is easy to underestimate. Model it on a fully-diluted basis before signing.

The Bottom Line

A SAFE and a convertible note both let you raise early money without pricing your company today — the difference is that a note is debt with interest and a deadline, and a SAFE strips those away. Pick based on your investors and market, get clear on the cap and discount, and keep a running cap table so conversion never surprises you. (For the round terms that come next, see our term sheet guide.)

When the documents arrive, upload your SAFE or note and ask AI to explain the cap, discount, and conversion terms in plain English before you sign — free to start.

Ready to automate your documents with AI?

Start free with AiDocX — AI contract drafting, meeting minutes, consultation notes, e-signatures, and more in one platform.

Get Started FreeMore from AiDocX Blog

Chat With Your Contract: How to Ask AI Questions About Any Document (2026)

Learn how to chat with a contract using AI — ask plain-English questions about clauses, deadlines, and risks instead of reading 30 pages. How it works, what to ask, and why a purpose-built tool beats pasting into ChatGPT.

Employee Stock Option Plans (ESOP) for Startups: Vesting, Pools, and Templates (2026)

A founder's guide to employee stock option plans — how options and vesting work, how big your option pool should be, the documents you need, and the mistakes that cost startups equity. With a free template workflow.

MSA vs SOW: Master Service Agreement vs Statement of Work (2026)

Confused about MSA vs SOW? A plain-English guide to what each document does, what goes in each, how they work together, and why separating them speeds up every deal — with a template workflow for agencies and freelancers.