Seed Round Fundraising Document Guide: From Term Sheet to Closing

Everything first-time founders need for seed fundraising: Term Sheet, SHA, investment agreements, due diligence documents, and closing checklist. Negotiation tips and common pitfalls included.

Seed Round Fundraising Document Guide: From Term Sheet to Closing

The seed round is the first formal fundraising experience for most founders. You've gotten a verbal commitment from an investor — maybe even a Term Sheet — but now what? What documents do you need, which clauses matter most, and how long does the whole process actually take? Nobody tells you upfront.

Ask your lawyer and they say "I'll handle it." Ask the investor and they say "just follow standard market practice." But once you're at the negotiation table, there's a mountain of details hiding behind "market practice" that you need to make judgment calls on.

Contracts and investor decks shouldn't take days — AiDocx lets you go from draft to signed in minutes. The key is knowing what to prepare, where to focus your energy, and what to move past quickly.

This guide breaks down the entire seed round process — from the first Term Sheet to closing — in chronological order. For each stage, we cover the required documents, key negotiation points, and common traps. Practical, not theoretical.

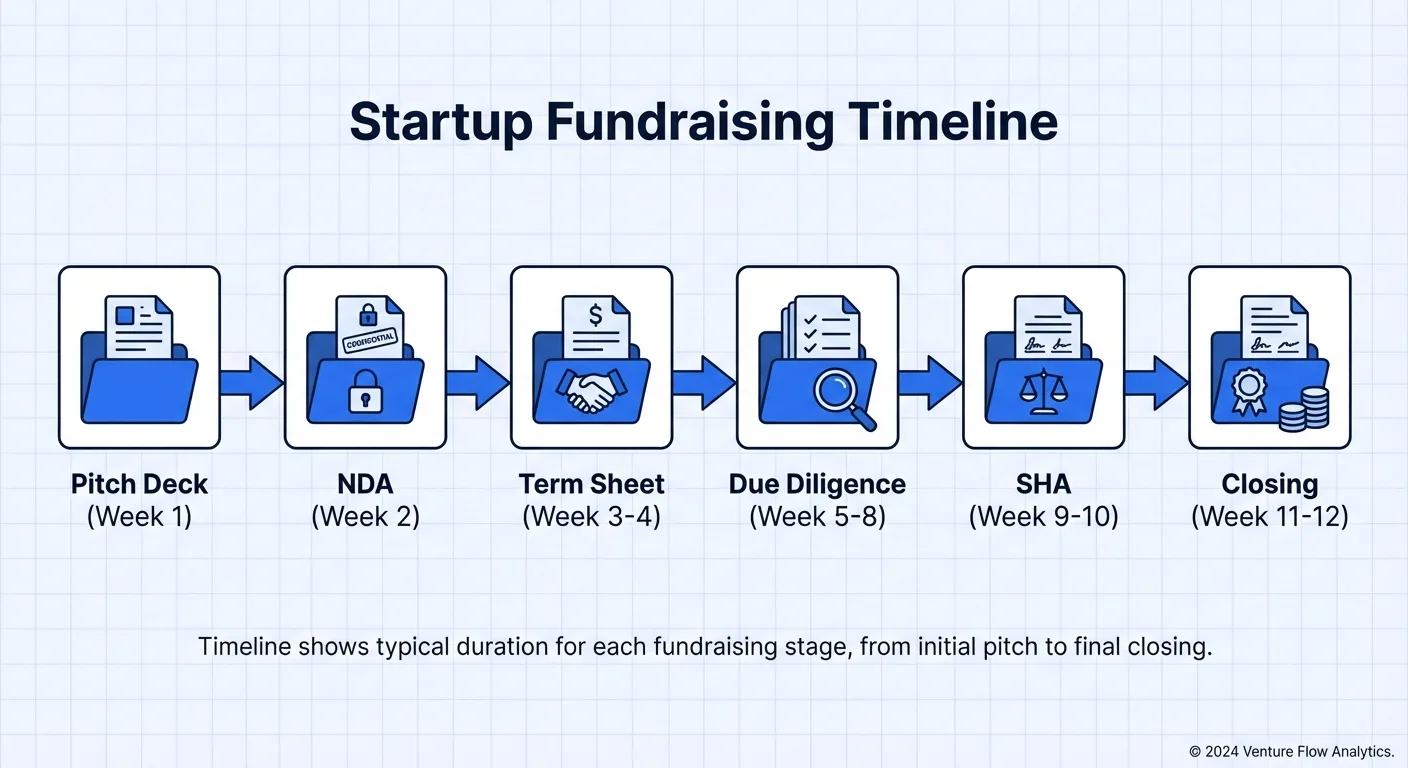

Overview: The Complete Fundraising Process

A typical seed round takes 6 to 12 weeks and breaks down into five stages.

- Term Sheet Negotiation (1–2 weeks)

- Due Diligence (2–4 weeks)

- Investment Agreement Execution (1–2 weeks)

- Shareholder Agreement & Corporate Governance (1–2 weeks)

- Closing & Registration (2–4 weeks)

Each stage has its own critical documents. Let's walk through them.

Stage 1: Term Sheet Negotiation

What This Stage Is

The Term Sheet (TS) is the investor's formal intent document. Most clauses aren't legally binding, but it sets the skeleton of the entire deal. If the TS negotiation falls apart, everything after it is irrelevant. If the TS is well-structured, 80% of the subsequent negotiation is already directionally set.

Document Checklist

- Term Sheet: Investor provides the first draft; founder reviews and requests clause-by-clause modifications

- Pitch Deck / Business Plan: Supporting evidence for the valuation negotiation

- Financial Projections: 12–24 month revenue and expense forecast

- Cap Table: Current shareholding structure for all shareholders, including option pool

Key Negotiation Points

Valuation and investment amount. Seed round post-money valuations vary widely — from $1M to $10M+ depending on market, traction, and geography. Investors evaluate your projections and traction data, but the actual valuation is driven by supply and demand. Multiple competing investors is a far stronger negotiation lever than any financial model.

Option pool. Investors almost always require an option pool to be created or expanded before their investment. 10–15% is the typical ask. The critical detail: the option pool dilutes the founder's shares, not the investor's. So calculate backward from your actual 12–18 month hiring plan. Don't just accept "industry standard 15%" without question.

Anti-dilution provisions. The most common form is Weighted Average Anti-dilution. If an investor requests Full Ratchet, a down round would reprice their shares at the lowest price — and the founder absorbs 100% of the dilution. At seed stage, insist on Broad-based Weighted Average.

Exclusivity period. Term Sheets typically include a 30–60 day no-shop clause preventing you from negotiating with other investors after signing. 30–45 days is reasonable. Anything over 60 days is clearly unfavorable for founders.

Practical Advice

The most common mistake at the TS stage is obsessing over the valuation number while overlooking clauses that affect your control long-term — liquidation preference multiples, board composition, veto rights. A high-valuation TS with 2x participating preferred can leave founders worse off at exit than a lower valuation with clean terms.

Ask an experienced founder to review the TS. One outside perspective is more valuable than reading it three times alone.

Stage 2: Due Diligence

What This Stage Is

After signing the TS, the investor begins due diligence (DD) — a comprehensive audit of your company before committing capital. Angel rounds might wrap up in a week, but VC seed rounds typically take 2–4 weeks.

Document Checklist

Corporate Documents:

- Certificate of incorporation / articles of organization

- Operating agreement / bylaws

- Board and shareholder meeting minutes (all)

- Current cap table and ownership structure

- Good standing certificates

Financial Documents:

- Last 2 years of financial statements (or since inception if younger)

- Bank statements (last 12 months)

- Tax returns (federal and state)

- Revenue and expense documentation for major contracts

Intellectual Property:

- Trademark registrations

- Patent filings and registrations

- Copyright registrations (software, content)

- Domain ownership verification

- IP assignment agreements from founders and key engineers

- Invention assignment agreements

Employment & HR:

- Founder employment agreements

- Employee census / org chart

- Contractor agreements (especially for technical work)

- Non-compete and non-solicitation agreements for key personnel

Legal:

- Prior investment documents (convertible notes, SAFEs, prior equity rounds)

- Material contracts (top 5–10 customer and vendor agreements)

- Office lease agreements

- Pending or threatened litigation disclosure

Common Due Diligence Issues

IP assignment gaps. If a co-founder built the core product before incorporating — or while employed elsewhere — the IP ownership chain may be unclear. This is the single most common deal-killer at the seed stage. Get clean IP assignment agreements signed before you even start fundraising.

Contractor vs. employee classification. Early startups often use contractors to save on benefits and payroll taxes. If those contractors are working full-time on core product features, there's misclassification risk. Investors will flag this and may require remediation before closing.

Informal side agreements. Verbal promises about equity splits between co-founders, informal advisory equity, or handshake revenue-sharing deals all surface during DD. If these aren't formalized, they can delay or kill the deal entirely.

Outstanding convertible instruments. If you've raised prior angel money via SAFEs or convertible notes, investors will scrutinize the conversion mechanics — especially valuation caps, discount rates, and MFN clauses. Make sure you can model exactly how these convert at the seed round price.

Practical Advice

The thing that trips up founders during DD isn't the volume of documents — it's the "things you thought were done but aren't."

Organize your documents before you start fundraising, not after you get a TS. A well-structured Virtual Data Room (VDR) signals professionalism and can shave 1–2 weeks off the DD timeline.

Stage 3: Investment Agreement Execution

What This Stage Is

Once DD passes, you enter the formal legal documentation and signing phase.

Document Checklist

- Stock Purchase Agreement (SPA): Investment amount, valuation, share price, closing conditions, representations and warranties, breach provisions

- Shareholders' Agreement (SHA): Rights and obligations between shareholders, preference rights, board composition, information rights, exit mechanisms

- Amended and Restated Certificate of Incorporation: Reflecting the new share class and investor rights

- Investor Rights Agreement: Information rights, anti-dilution, pro-rata rights, co-sale rights, drag-along rights

- Representations and Warranties Certificate: Founder's written guarantees about company status

For US-based deals, the NVCA (National Venture Capital Association) model documents are the standard starting point. Using these templates significantly reduces legal costs and negotiation time.

Key Negotiation Points

Liquidation Preference. The seed-stage standard is 1x non-participating preferred. The investor gets their money back first at exit, then remaining proceeds are distributed pro-rata. If the investor demands participating preferred, they get their money back AND participate in the remaining distribution — effectively "double-dipping." At seed stage, non-participating is the principle to defend.

Veto Rights. Investors will request consent rights (veto power) on major decisions. Typical items include:

The following actions shall require the prior written consent of investors holding a majority of the preferred stock:

(1) Issuance of new shares, options, warrants, or convertible securities

(2) Acquisition or disposal of assets exceeding $[___]

(3) Related-party transactions

(4) Amendment of charter provisions related to investor preference rights

(5) Dissolution, liquidation, or filing for bankruptcy

(6) Mergers, acquisitions, or reorganizations involving a change of control

5–7 veto items is reasonable. If the investor demands 15+ items (including annual budget approval, officer appointments, routine borrowing), your operational autonomy is severely constrained. Push back or negotiate dollar thresholds.

Founder restrictions. Investment agreements almost always include founder full-time commitment, non-compete, and share transfer restrictions. Check that the non-compete scope isn't unreasonably broad ("all fields related to the company's business") and that share transfer restrictions include exceptions for estate planning and tax restructuring.

Practical Advice

Investment agreement negotiation is lawyer-led on both sides. But a common founder mistake is delegating entirely to counsel without understanding the terms yourself. Lawyers assess legal risk — but they don't understand your business context. A performance-milestone clause that's "legally acceptable" might be completely misaligned with your growth trajectory.

Also, don't concede important terms to speed up the process. The investment agreement isn't a one-time document — it governs your company's life until it's superseded by the next round. A concession today to save two days can become an unsolvable governance problem three years from now.

Stage 4: Shareholder Agreement & Corporate Governance

What This Stage Is

Before closing, investors typically require the company to formalize its option plan and establish governance structures.

Document Checklist

Stock Option Plan:

- Board resolution approving the equity incentive plan

- Equity Incentive Plan document

- Form of stock option agreement (individual grant template)

- Option grant ledger / register

- 409A valuation (for US companies)

Governance:

- Amended bylaws (reflecting board changes, investor consent rights)

- Board seat appointment documentation

- Board observer rights agreement (if applicable)

- D&O insurance confirmation

Stock Options at Seed Stage

For US companies, stock options are typically granted under an equity incentive plan approved by both the board and shareholders. The plan specifies the total share pool, exercise price methodology, vesting schedules, and tax treatment (ISO vs. NSO).

The exercise price must be at or above fair market value (FMV) to avoid adverse tax consequences. For private companies, this requires a 409A valuation — an independent appraisal typically conducted annually or after significant events (like a funding round). A common mistake is granting options before the 409A is updated post-investment, which can create tax problems for employees.

Standard vesting is 4 years with a 1-year cliff: nothing vests for the first year, then 25% vests at the cliff, and the remaining shares vest monthly or quarterly over the following 3 years.

Practical Advice

Many investors at the seed stage won't require a formal board seat — they'll request a board observer role or simply information rights. But if they do request a board seat, negotiate carefully: a 3-person board with one investor seat and one independent seat leaves the founder in a precarious position if the independent sides with the investor.

The standard seed-stage board is 3 members: 2 founder-designated seats and 1 investor seat. Protect this ratio.

Stage 5: Closing & Registration

What This Stage Is

Once all documents are signed, you enter the closing phase. The core is simple: the investor wires the investment amount, the company issues shares, and the registration updates are filed.

Sounds simple, but this is often the stage with the most delays.

Document Checklist

Closing Documents:

- Closing certificate

- Wire transfer confirmation

- Stock certificates or book-entry confirmation

- Signed copies of all transaction documents

Filing & Registration:

- Amended and Restated Certificate of Incorporation (filed with Secretary of State)

- Form D filing with SEC (within 15 days of first sale)

- State blue sky filings (as applicable)

- Updated cap table reflecting the new round

- 83(b) election reminders for any founders receiving restricted stock

Conditions Precedent

Investment agreements specify closing conditions that must be satisfied before the investor wires funds. Typical conditions include:

- Company's representations and warranties remain true and accurate at closing

- Required government filings and approvals completed

- All IP properly assigned to the company

- Option plan adopted and operational

- Key employee agreements executed (employment, non-compete, IP assignment)

- No Material Adverse Change (MAC) since signing

- Legal opinion letter from company counsel

If specific conditions can't be met by closing, the investor may issue a written waiver. But the best approach is to satisfy all conditions ahead of time.

Practical Advice

The most important principle at closing: do not file irreversible corporate changes before the investment funds are wired. The correct sequence is: sign documents → satisfy conditions → receive wire → file amendments. If you file the amendment adding the investor as a shareholder and the wire never arrives, you're in an extremely complex legal dispute.

Complete Timeline

| Stage | Duration | Key Documents | Lead |

|---|---|---|---|

| TS Negotiation | 1–2 weeks | Term Sheet, Pitch Deck, Cap Table | Founder + Investor |

| Due Diligence | 2–4 weeks | Corporate / Financial / Legal / IP docs | Founder + Investor counsel |

| Investment Agreement | 1–2 weeks | SPA, SHA, Amended Charter | Both counsels |

| Options / Governance | 1–2 weeks | Option plan, Bylaws | Founder counsel |

| Closing / Filing | 2–4 weeks | Closing certificate, Filings | Founder + corporate counsel |

Total: 7–14 weeks

Key Clause Reference (Copy-Paste Ready)

Certain high-impact clauses appear repeatedly in investment documents. Below are standard formulations founders can reference or adapt directly.

Anti-Dilution — Broad-Based Weighted Average (Founder-Friendly Version)

In the event the Company issues shares at a per-share price lower than the Original Issue Price ("Down Round"), the Conversion Price of the Preferred Stock shall be adjusted according to the following Broad-Based Weighted Average formula:

Adjusted Conversion Price = Original Conversion Price × (Outstanding Shares + Shares Issuable at Original Conversion Price) / (Outstanding Shares + Shares Actually Issued)

"Outstanding Shares" shall include all shares of Common Stock, all shares of Common Stock issuable upon conversion of outstanding Preferred Stock, and all shares issuable upon exercise of outstanding options. Unallocated shares in the option pool shall be excluded from the calculation.

Note: If the investor proposes Narrow-based Weighted Average or Full Ratchet, founder dilution increases significantly. Broad-based Weighted Average should be the baseline for seed rounds.

Liquidation Preference — Two Versions Compared

Version 1: 1x Non-Participating (Founder-Friendly, Seed Standard)

Upon any Liquidation Event (including a Deemed Liquidation Event), the holders of Preferred Stock shall be entitled to receive, prior to any distribution to holders of Common Stock, an amount per share equal to the Original Issue Price (plus any declared but unpaid dividends). After payment of the Preferred Stock preference amount, the remaining assets shall be distributed to holders of Common Stock on a pro-rata basis.

Version 2: 1x Participating (Investor-Friendly, Founder Beware)

…After payment of the Preferred Stock preference amount, the holders of Preferred Stock shall participate alongside holders of Common Stock in the distribution of remaining assets on an as-converted pro-rata basis, until the aggregate amount received by holders of Preferred Stock equals [___]x the Original Issue Price.

Key difference: In a modest exit (say $10M), participating preferred can dramatically reduce what the founder actually receives. Always model both versions with your actual investment amount and ownership percentage.

Due Diligence VDR Folder Structure (Ready to Share with Investors)

Organizing your VDR with this structure lets investor counsel complete their initial review within 1–2 weeks. Without organization, the same review stretches to 4–6 weeks.

01_Corporate/

- Certificate of Incorporation (current)

- Bylaws

- Board & Shareholder Minutes (all)

- Good Standing Certificates

02_Cap_Table/

- Current Cap Table (including all convertible instruments)

- Prior Investment Documents (SAFEs, notes, equity)

- Option Grant Ledger

03_Financial/

- Financial Statements (last 2 years)

- Bank Statements (last 12 months)

- Tax Returns (federal and state)

- Material Contract Revenue Documentation

04_Intellectual_Property/

- Trademark Registrations

- Patent Filings

- Copyright Registrations

- Domain Ownership

- IP Assignment Agreements

05_Contracts/

- Top Customer Agreements

- Vendor Agreements

- Lease Agreements

- Strategic Partnership Agreements

06_Employment/

- Founder Employment Agreements

- Key Employee Agreements

- Contractor Agreements

- Non-Compete / NDA Agreements

- IP Assignment Confirmations

07_Other/

- Government Permits & Licenses

- Insurance Policies

- Litigation Disclosure (if any)

You can use AiDocX's VDR feature to share these documents securely with your investment team — complete with granular access controls, viewer tracking, and dynamic watermarking.

Five Principles to Remember

No matter where you are in the fundraising process, keep these five principles in mind.

First, hire a lawyer early. Seed-round legal fees typically range from $5K to $30K. That may feel expensive, but a flawed investment agreement creates losses 100x the legal cost. Choose a firm with VC fundraising experience — not the real estate lawyer your friend recommended.

Second, run workstreams in parallel. Don't wait for DD to finish before starting the investment agreement. Don't wait for the agreement to finalize before amending your charter. Running these concurrently can compress the total timeline by 2–3 weeks.

Third, maintain document discipline. You'll be managing dozens of documents across multiple versions throughout the fundraising process. If you're trading files over email and messaging apps, you'll lose track of the final signed version by closing. Use a VDR or document management tool from the TS stage onward to keep everything in one place.

Fourth, document every verbal agreement in writing. Many fundraising agreements happen over calls and meetings. After every important conversation, immediately send a summary via email and get the other party's confirmation. "You said that on the call" means nothing without a written record.

Fifth, maintain deal momentum. The biggest enemy of fundraising is delay. Every day that slips increases the odds of unexpected variables: market shifts, internal investor committee changes, competitor news. Once you have a TS, push at full speed to close within 6–8 weeks.

Seed fundraising isn't easy. But it's not mysterious either. When you know exactly what to do at each stage — which documents to prepare, which traps to avoid — the "unknown anxiety" transforms into a "manageable project." Use this guide as your project management checklist, and you'll be heading in the right direction.

FAQ

How long does a typical seed round take from Term Sheet to closing?

Most seed rounds close in 7–14 weeks. The biggest variables are DD complexity and legal negotiation speed. Running workstreams in parallel can compress this to 6–8 weeks.

What's the most important clause to negotiate in a Term Sheet?

Liquidation preference structure. A 1x non-participating preferred is standard at seed stage. Participating preferred or high multiples can significantly reduce founder payouts at exit — often more impactful than the valuation number itself.

Do I need a lawyer for a seed round?

Yes. Even if you're using NVCA model documents or standard SAFEs, having experienced startup counsel review the terms is essential. The cost ($5K–$30K) is trivial compared to the governance problems a poorly negotiated agreement can create.

What's the difference between a SAFE and a priced seed round?

A SAFE (Simple Agreement for Future Equity) defers valuation to the next priced round, while a priced seed round sets an explicit valuation and issues preferred stock immediately. SAFEs are faster and cheaper but give founders less certainty about dilution until conversion.

How should I organize documents for due diligence?

Use a Virtual Data Room (VDR) with a clear folder structure: Corporate, Cap Table, Financial, IP, Contracts, Employment, and Other. Having documents organized before DD starts can cut the process from 4–6 weeks down to 2 weeks.

Ready to automate your documents with AI?

Start free with AiDocX — AI contract drafting, meeting minutes, consultation notes, e-signatures, and more in one platform.

Get Started FreeMore from AiDocX Blog

Anti-Dilution Provisions Explained: What Founders Must Know (2026)

A founder's guide to anti-dilution provisions in investment agreements — how full ratchet and weighted-average protection work, what happens in a down round, and how each option affects your equity. With a worked calculation and ready-to-use clause templates.

Pre-A Round Fundraising: The Complete Document Checklist for Founders (2026)

What a pre-A (bridge) round is, how it differs from seed and Series A, how it's valued, and the full document checklist — term sheet, cap table, financial model, data room, and investment agreement — you need to close it fast.

Chat With Your Contract: How to Ask AI Questions About Any Document (2026)

Learn how to chat with a contract using AI — ask plain-English questions about clauses, deadlines, and risks instead of reading 30 pages. How it works, what to ask, and why a purpose-built tool beats pasting into ChatGPT.