Anti-Dilution Provisions Explained: What Founders Must Know (2026)

A founder's guide to anti-dilution provisions in investment agreements — how full ratchet and weighted-average protection work, what happens in a down round, and how each option affects your equity. With a worked calculation and ready-to-use clause templates.

Anti-Dilution Provisions Explained: What Founders Must Know

You raise your Series A at a $100M valuation. The investor puts in $20M for 20% of the company, and you walk away still owning 60%. A year later the market turns, and your Series B prices at $50M. You assume you still hold most of the company — until your lawyer explains that the anti-dilution clause in your Series A agreement just quietly cut your stake to 46%.

That is not a hypothetical. Every year, founders sign a term sheet without reading the anti-dilution language closely, and only discover what it costs when a down round actually happens. By then the mechanics are locked in.

This guide is a plain-English, founder-focused walk through anti-dilution protection: what it is, why investors insist on it, the difference between full ratchet and weighted-average formulas, a concrete calculation, clause templates you can adapt, how it interacts with your other terms, and how to negotiate it. If you're preparing a seed round or reviewing a term sheet, this could save you several points of ownership.

What Is an Anti-Dilution Provision?

An anti-dilution provision protects an investor's ownership when the company later sells stock at a lower price per share than they paid. The logic is simple: if you issue new shares below the earlier round's price (a down round), the earlier investor's preferred stock converts into common stock at an adjusted, lower price — which gives them more shares to compensate for the drop in value.

Crucially, those extra shares don't appear from nowhere. They dilute everyone who isn't protected — mainly founders and the employee option pool.

Why Investors Want It

An investor who buys in at a high valuation is taking a bet on your projections. Anti-dilution is essentially price insurance against that bet going wrong:

- Down-round compensation. If the company's value falls, the early investor isn't stuck absorbing the full loss at their original high price.

- A hedge on information asymmetry. Investors rely on the numbers and plans you present. Anti-dilution reduces their cost if reality lands below the forecast.

- Standard practice. Nearly every institutional priced round includes some form of anti-dilution protection.

This is not a "greed clause." It's a decades-old, standard mechanism in venture financing. The real questions are which type you agree to and how the parameters are set — because those choices swing outcomes dramatically.

The Three Anti-Dilution Mechanisms

There are three common structures, and their impact on founders ranges from mild to severe.

| Dimension | Full Ratchet | Broad-Based Weighted Average | Narrow-Based Weighted Average |

|---|---|---|---|

| How it adjusts | Conversion price drops to the new round's price | Adjusted by a weighted formula | Same formula, but a smaller share base |

| Impact on founders | Severe — full adjustment even on a tiny raise | Mild — scales with the size of the down round | Moderate — harsher than broad-based |

| How common | Rare, only with very strong investor leverage | Most common — the market standard | Occasional |

| Founder-friendliness | ★☆☆☆☆ | ★★★★☆ | ★★★☆☆ |

Full Ratchet

The harshest version for founders. No matter how small the down round is, the earlier investor's conversion price drops all the way to the new, lower price. If they bought at $10 per share and you later sell a small amount at $5, their conversion price becomes $5 — effectively doubling their shares. Founders and employees absorb the entire cost.

Broad-Based Weighted Average

The most common structure in the market. It uses a weighted formula to split the impact of the down round between old and new shareholders. The smaller the down round relative to the company, the smaller the adjustment.

New conversion price = Old conversion price × (A + B) / (A + C)

A = shares outstanding before the down round, fully diluted

(all common, all preferred as-converted, and granted options)

B = shares the new money would have bought at the OLD price

C = shares actually issued in the down round

Narrow-Based Weighted Average

The same formula, but A is defined more narrowly — typically only the outstanding preferred stock, excluding common and the option pool. A smaller denominator means a bigger adjustment, so it favors the investor. It sits between broad-based and full ratchet.

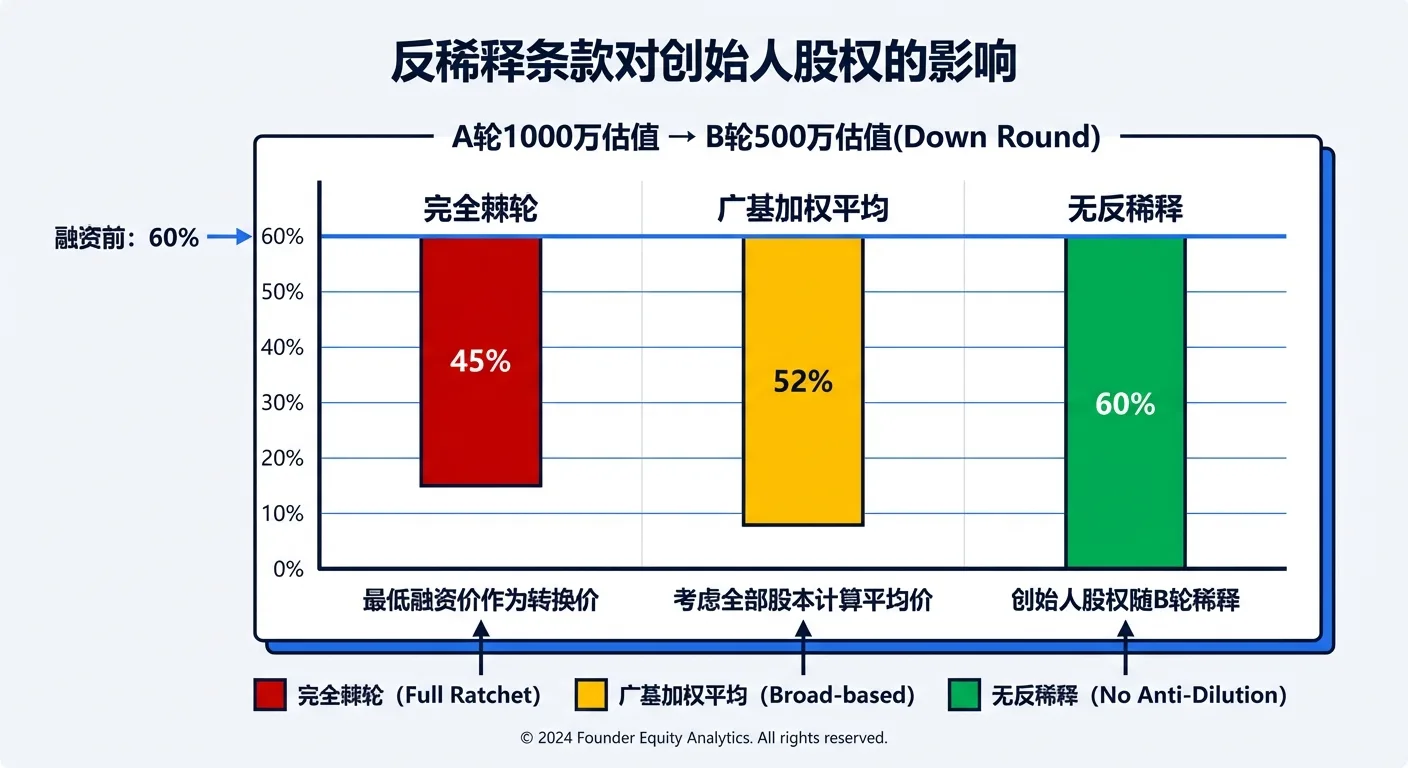

A Worked Example

Numbers make the difference obvious. Here's a simple setup.

Starting Point

| Item | Value |

|---|---|

| Pre-money valuation (Series A) | $100M |

| Series A raise | $20M |

| Investor ownership | 20% |

| Price per share | $10.00 |

| Total shares (post-A) | 10,000,000 |

| Founder ownership | 60% (6,000,000 shares) |

| Option pool | 20% (2,000,000 shares) |

The Down Round

Series B prices at a $50M valuation — $5.00 per share — raising $5M and issuing 1,000,000 new shares.

Results Under Each Mechanism

| Metric | No Anti-Dilution | Full Ratchet | Broad-Based WA | Narrow-Based WA |

|---|---|---|---|---|

| Series A conversion price | $10.00 | $5.00 | $9.09 | $8.33 |

| Series A shares | 2,000,000 | 4,000,000 | 2,200,000 | 2,400,000 |

| Total shares (post-B) | 11,000,000 | 13,000,000 | 11,200,000 | 11,400,000 |

| Series A ownership | 18.2% | 30.8% | 19.6% | 21.1% |

| Founder ownership | 54.5% | 46.2% | 53.6% | 52.6% |

| Founder loss vs. baseline | — | −8.3 pts | −0.9 pts | −1.9 pts |

Broad-based weighted average math:

A = 10,000,000 (all shares, fully diluted)

B = $5,000,000 ÷ $10 = 500,000

C = $5,000,000 ÷ $5 = 1,000,000

New price = $10 × (10,000,000 + 500,000) / (10,000,000 + 1,000,000)

= $10 × 10,500,000 / 11,000,000 = $9.09

New Series A shares = $20,000,000 ÷ $9.09 = 2,200,000

The takeaway: in the same down round, full ratchet costs the founders 8.3 points of ownership, while broad-based weighted average costs less than 1 point. That is why the type of anti-dilution — not just its presence — is one of the most consequential choices in your term sheet.

Ready-to-Use Clause Templates

Adapt these to your deal, and review them alongside your shareholder agreement.

Broad-Based Weighted Average

Section X — Anti-Dilution Adjustment. If, after the closing of this round, the Company issues additional equity securities at a price per share less than the Original Issue Price of the Preferred Stock (a "Dilutive Issuance"), the Conversion Price of such Preferred Stock shall be adjusted as follows:

New Conversion Price = Original Conversion Price × (A + B) / (A + C)

where:

- A = the total number of shares outstanding immediately before the Dilutive Issuance, on a fully-diluted basis (including all common stock, all preferred stock on an as-converted basis, and all granted but unexercised options);

- B = the number of shares the total consideration of the Dilutive Issuance would have purchased at the Original Conversion Price;

- C = the number of new shares actually issued in the Dilutive Issuance.

The adjustment takes effect automatically upon each Dilutive Issuance.

Full Ratchet

Section X — Full-Ratchet Anti-Dilution Adjustment. If, after the closing of this round, the Company issues additional equity securities at a price per share less than the Original Issue Price of the Preferred Stock (a "Dilutive Issuance"), the Conversion Price of such Preferred Stock shall automatically be adjusted to equal the lowest price per share at which such new equity securities are issued in the Dilutive Issuance.

Pay-to-Play

Section X — Pay-to-Play. In connection with any qualifying financing (a "Qualified Financing"), each holder of Preferred Stock shall participate pro rata to its holdings. Any holder that fails to participate at least to its required pro-rata share (measured on a fully-diluted basis) shall have its Preferred Stock automatically converted into common stock, thereby forfeiting its liquidation preference, anti-dilution rights, and other preferential rights under this Agreement.

Exceptions and Carve-Outs

Section X — Excluded Issuances. The following issuances do not constitute a "Dilutive Issuance" and do not trigger any anti-dilution adjustment:

(a) options or restricted shares issued to employees, directors, or advisers under a board-approved equity incentive plan, up to [15]% of the Company's fully-diluted capitalization; (b) shares issued as a result of a stock split, combination, or stock dividend; (c) shares issued upon the exercise or conversion of securities already outstanding at the closing of this round; (d) any issuance for which anti-dilution adjustment is waived in writing by holders of a majority of the Preferred Stock; (e) shares issued in connection with a strategic commercial partnership approved by the board (including the investor director).

How It Interacts with Your Other Terms

Anti-dilution never operates in isolation. Three interactions matter most.

With the Liquidation Preference

Your liquidation preference sets who gets paid first in a sale or wind-down. Once anti-dilution triggers, the investor holds more converted shares — so the two terms compound. Participating preferred plus full ratchet is the worst combination for founders: the investor takes their money back first and shares in the rest at a higher, adjusted stake. If you're forced to accept a full ratchet, push hard to keep the preference at a plain 1x non-participating.

With Pro-Rata Rights

Pro-rata rights let an investor maintain their ownership in future rounds. The problem: some investors want anti-dilution protection without putting fresh money into the down round. A pay-to-play provision solves this — investors who don't participate in the next round lose their anti-dilution protection.

With Founder and Employee Equity

The new shares from an anti-dilution adjustment come from everyone unprotected — founders and the option pool. A down round therefore erodes your team's option value, not just your own stake. Plan your cap table with a buffer, and be explicit with your team about this risk when you grant options.

Founder Negotiation Strategies

- Insist on broad-based weighted average. The overwhelming majority of venture deals use it. If an investor demands a full ratchet, treat it as a warning sign about how the rest of the relationship will go.

- Ask for pay-to-play. It's founder-friendly: investors only keep their protection if they keep backing you. It stops passive investors from diluting you without writing a check.

- Negotiate a price floor. Cap the adjustment — for example, the conversion price can't fall below 50% of the original. This limits the damage of an extreme down round.

- Add a time limit. Anti-dilution can be scoped to issuances within, say, 24–36 months of closing. After that, the protection lapses.

- Broaden the carve-outs. The wider your list of excluded issuances — option grants, note conversions (SAFEs and convertible notes), bridge financing, strategic partnerships — the less often anti-dilution can trigger at all.

Frequently Asked Questions

If I'm confident I'll never do a down round, does anti-dilution matter? Yes. Market cycles, macro shocks, and slower-than-planned growth all cause down rounds that no founder plans for. Beyond that, the type of anti-dilution on your cap table affects whether future investors want to come in — new investors evaluate how existing protections will treat them.

Can I just have no anti-dilution at all? In theory, yes; in practice, almost never. It's a baseline expectation for institutional investors. With strong leverage (multiple competing term sheets) you can win founder-friendly terms — broad-based weighted average, pay-to-play, wide carve-outs — but removing it entirely is extremely rare.

Does the employee option pool get diluted too? Yes. Anti-dilution shares dilute every unprotected holder, including the pool — which means a down round quietly reduces the value of your team's options. Factor this in when you size and grant the pool.

Do SAFE or convertible note conversions trigger anti-dilution? It depends on your carve-outs. Well-drafted clauses usually exclude conversions of instruments that were already outstanding, since their terms were fixed when issued. But if a note converts below the prior round's price and isn't explicitly excluded, it can trigger an adjustment. See our SAFE vs convertible note guide.

A down round already happened — what can I do now? A few options: negotiate a partial or full waiver of the adjustment in exchange for cooperating on the round; ask the new investor's terms to limit the old investors' anti-dilution rights; refresh the option pool to partly restore your team's stake; or, if valuation recovers, reset or remove the earlier adjustment in a future round.

The Bottom Line

Anti-dilution looks like a technical footnote, but it decides how much of your company you keep in the exact moment it hurts most — when the valuation drops. The gap between full ratchet and broad-based weighted average can be the difference between still leading your company and becoming a minority shareholder. Insist on weighted average, ask for pay-to-play, widen the carve-outs, and always model the worst case before you sign.

When the term sheet or investment agreement lands, upload it to AiDocX and ask AI to explain the anti-dilution clause — full ratchet or weighted average, what it costs you, and where to push back — free to start.

Ready to automate your documents with AI?

Start free with AiDocX — AI contract drafting, meeting minutes, consultation notes, e-signatures, and more in one platform.

Get Started FreeMore from AiDocX Blog

Pre-A Round Fundraising: The Complete Document Checklist for Founders (2026)

What a pre-A (bridge) round is, how it differs from seed and Series A, how it's valued, and the full document checklist — term sheet, cap table, financial model, data room, and investment agreement — you need to close it fast.

Chat With Your Contract: How to Ask AI Questions About Any Document (2026)

Learn how to chat with a contract using AI — ask plain-English questions about clauses, deadlines, and risks instead of reading 30 pages. How it works, what to ask, and why a purpose-built tool beats pasting into ChatGPT.

Employee Stock Option Plans (ESOP) for Startups: Vesting, Pools, and Templates (2026)

A founder's guide to employee stock option plans — how options and vesting work, how big your option pool should be, the documents you need, and the mistakes that cost startups equity. With a free template workflow.