Pre-A Round Fundraising: The Complete Document Checklist for Founders (2026)

What a pre-A (bridge) round is, how it differs from seed and Series A, how it's valued, and the full document checklist — term sheet, cap table, financial model, data room, and investment agreement — you need to close it fast.

Pre-A Round Fundraising: The Complete Document Checklist for Founders

You've run for a year on your seed money. The product shipped, you have a few hundred paying users, and revenue is finally moving. On the original plan you'd be raising your Series A about now — but the numbers aren't yet where Series A investors expect them to be. You have maybe six to nine months of runway left, and waiting isn't free. That's the moment founders reach for a pre-A round.

The pre-A (also called pre-Series A or a bridge round) fills the widening gap between seed and Series A. It isn't a bigger seed round, and it isn't a smaller Series A — it's a distinct financing stage with its own logic, its own valuation math, and its own document requirements. Founders who treat it as "seed with bigger numbers" get passed on; founders who over-engineer it like a full Series A waste weeks they don't have.

This guide covers what the pre-A round is, when to raise one, how it's valued, the complete document checklist, what investors diligence at this stage, and the mistakes that quietly kill these rounds.

What Is a Pre-A Round?

A pre-A round is a bridge financing that sits between your seed round and your Series A. Its core positioning is simple: you've used your seed capital to validate the product (early product-market-fit signals), but you haven't yet hit the scale that Series A investors underwrite.

Investors at this stage are backing a company that has finished "zero to one" and is just starting "one to ten." You no longer have to prove the business model works — the seed stage answered that. What you have to prove is that the growth engine exists and just needs more fuel to accelerate. If you're still "exploring direction" after you take the money, you don't need a pre-A; you need to rethink your seed.

Because of that, pre-A capital tends to have a very specific job: expand acquisition, fill a few key hires, and build a repeatable sales motion — enough to reach the metrics that unlock a Series A in the next 12–18 months. (For the round that comes before this one, see our seed round fundraising document guide.)

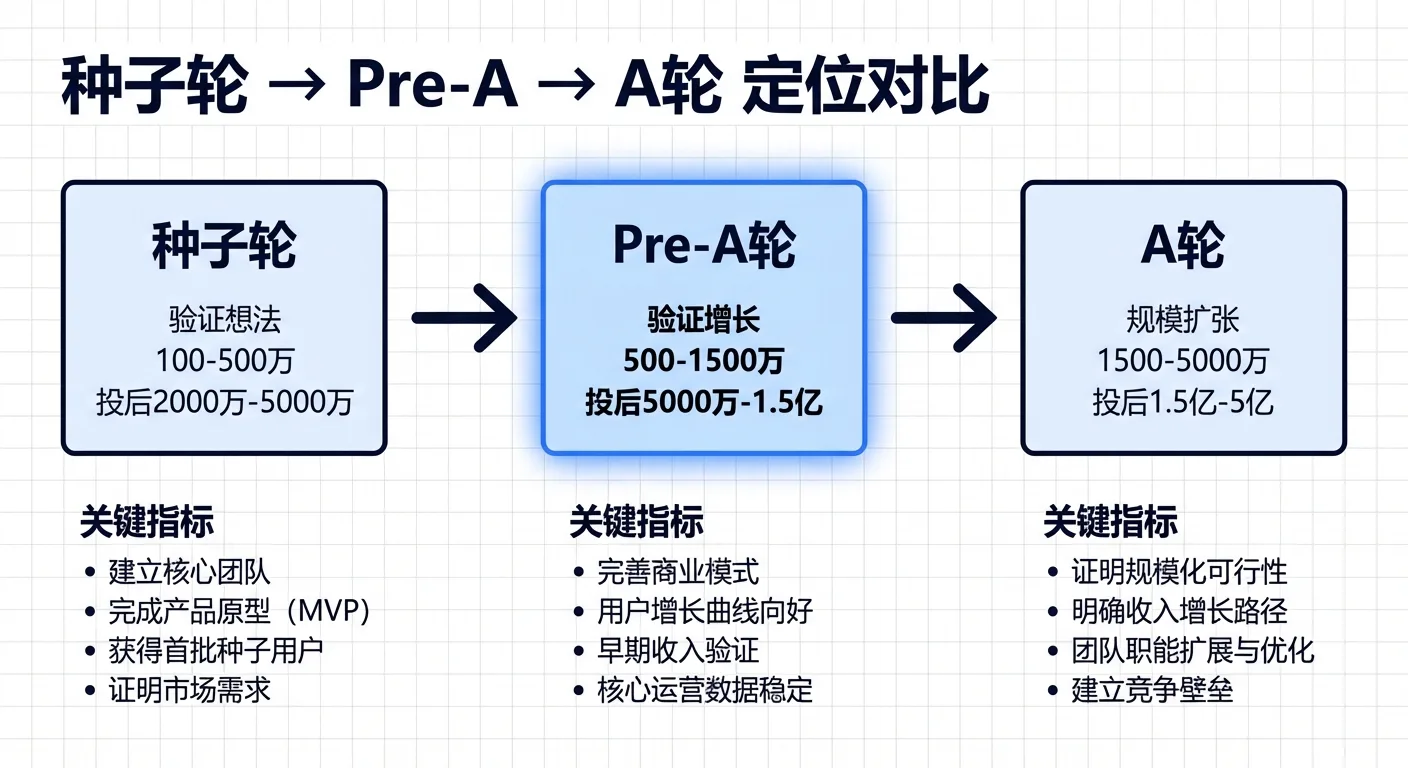

Seed vs Pre-A vs Series A: The Real Differences

The clearest way to understand a pre-A is to place it between the two rounds it bridges. Rough, jurisdiction-neutral parameters for 2026:

| Dimension | Seed | Pre-A | Series A |

|---|---|---|---|

| Raise size | Small | Medium | Large |

| What's underwritten | Team + idea + prototype | PMF signal + early revenue + growth trend | Scalable revenue + repeatable growth model |

| Revenue expectation | None required | Early, growing recurring revenue | Substantial, predictable recurring revenue |

| Typical dilution | 10–20% | 10–15% | 15–25% |

| Instrument | SAFE / convertible note | SAFE/note or priced preferred | Priced preferred equity |

| Lead investor | Angels / seed funds | Early-stage VCs / seed+ funds | Institutional VCs |

| Diligence depth | Light | Moderate | Deep |

| Document complexity | Simple (templates fine) | Moderate | High (counsel required) |

| Time to close | 4–8 weeks | 6–10 weeks | 8–16+ weeks |

The key takeaway: the pre-A's document complexity sits between the two. You can no longer use the stripped-down seed paperwork, but you don't need the full institutional legal architecture of a Series A either.

When Do You Actually Need a Pre-A?

Not every company should raise a pre-A. It makes sense in a few clear situations:

Your metrics are growing but not yet at Series A bar

Revenue is climbing at a healthy rate, but a Series A lead expects meaningfully more. You need six to twelve months of runway to get there.

Your seed money is running low

You have six to nine months of cash left. If you start a Series A now, the typical three-to-six-month cycle means you'll run out before closing. A pre-A closes faster (often 6–10 weeks) and buys you buffer.

You need to validate a specific hypothesis

You've found PMF but the model still needs tuning — pricing, an acquisition channel, or your ideal customer profile. A pre-A funds those experiments before the A.

The market window is short

In fast-moving categories (AI applications, vertical SaaS), waiting until your metrics are "A-ready" can mean missing the window entirely. A pre-A gets ammunition into your hands sooner.

The Complete Pre-A Document Checklist

Pre-A preparation is a clear step up from seed. Here's the full set.

1. Updated pitch deck

Seed sells vision and team; pre-A sells data and execution. Your deck should show the validated problem, real product screens and user feedback (not mockups), traction data (recurring revenue curve, retention, CAC/LTV), a repeatable growth model, a concrete use-of-funds plan, and the milestones between this round and your Series A.

2. Financial model

Move beyond a simple income projection. Investors expect actuals vs. your seed-stage forecast, unit economics (CAC, LTV, payback period, gross margin), an 18–24 month projection in conservative/base/optimistic scenarios, a monthly cash-flow statement, and a post-raise runway calculation showing when you'll need the A.

3. Traction dashboard

A static screenshot won't cut it. Prepare a live (or at least weekly-updated) dashboard: MAU and paying-user trends, MRR/ARR curve, churn and net revenue retention, acquisition channel mix and efficiency, and core product-usage metrics.

4. Updated cap table

The cap table gets more complex here because it must reflect your seed investors' holdings, options granted and exercised, the dilution impact of the new pre-A money, and any option-pool top-up. If your employee stock option plan needs expanding before the round, plan the pool math now — investors almost always want it done pre-money.

5. Term sheet

The term sheet is the skeleton of the deal — more detailed than a seed term sheet, less exhaustive than a Series A. Get the mechanics right on valuation, option pool, board rights, anti-dilution, and information rights. (Our startup term sheet template guide walks through each clause.)

6. Investment / subscription agreement

The binding contract that implements the term sheet: share subscription (or note/SAFE) agreement, representations and warranties, closing conditions, and investor rights. This is where the term sheet becomes enforceable.

7. Board & shareholder consents

Board resolutions authorizing the raise and any amended shareholder agreement. Review your existing shareholder agreement for pro-rata, consent, and anti-dilution rights your seed investors may already hold — those clauses shape what you can offer the new lead.

8. Disclosure schedule

A structured list of exceptions to the reps and warranties (existing debts, litigation, IP encumbrances, material contracts, key-person dependencies). Preparing it early surfaces problems before diligence does.

9. Supporting data room

- Corporate formation and registration documents

- Seed-round investment and shareholder agreements (for the new investor to review)

- IP evidence (patents, trademarks, software copyrights)

- Key-team resumes and option agreements

- Customer contracts or letters of intent (to substantiate revenue)

- Compliance documents (privacy policy, industry licenses)

Assemble these in an organized data room before you open the round, not when the first investor asks.

How Pre-A Rounds Are Valued

Valuation is the central negotiation. At the pre-A stage, revenue is usually too thin to support a purely financial model, so investors blend several methods.

Revenue multiple

The most direct approach for companies with steady recurring revenue: post-money valuation = ARR × multiple. The multiple varies widely with growth rate and category.

Comparable companies

Reference what similar-stage companies in your category raised at. Sources: public funding databases, investor market data, and peer founders.

Milestone-based valuation

Rather than revenue, this looks at which risk-reducing milestones you cleared since seed:

| Milestone | Rough valuation contribution |

|---|---|

| Product launched | + |

| First paying customers | ++ |

| Positive unit economics | +++ |

| Repeatable acquisition channel | ++ |

| Key hires in place | + |

| Strategic partnership / anchor customer | ++ |

A common heuristic: take your seed post-money and apply a risk-reduction multiple. If most of these milestones are done, a 1.5×–3× step-up from your seed valuation is typical.

The practical reality

Whatever method you use, price is ultimately set by supply and demand. If two or three funds are competing, valuation rises naturally; if you have one option, your leverage is thin. Line up five to ten potential investors before you start so you always have an alternative at the table.

If you're choosing between a priced round and a SAFE or convertible bridge, remember the trade-off: a priced pre-A sets a clean valuation and gives the new investor preferred rights, while a SAFE/note bridge is faster and cheaper but defers valuation to the A — watch the cap and discount so conversion doesn't over-dilute you.

What Pre-A Investors Diligence

Unlike seed investors, pre-A investors have a concrete evaluation framework:

- Product-market fit signals. Are users retaining? Is there organic growth? A simple test: if your product vanished tomorrow, would users be upset?

- Repeatability of growth. Seed growth often comes from the founder's network or one-off PR. Pre-A investors want at least one channel you can pour money into and get predictable output.

- Unit economics trend. Even if you're losing money, is CAC falling, LTV rising, LTV/CAC above ~3, and payback shrinking?

- Execution. How much of what you promised at seed did you deliver? What key decisions did you make, and why?

- A clear path to Series A. They need to believe this money gets you to a fundable A in 12–18 months. Be ready to state exactly what metrics trigger the A raise.

Common Pre-A Mistakes

Using seed materials for a pre-A. "It's all early-stage, just change the numbers" gets you passed on. Your narrative has to shift from what we're going to do to what we've already done and how we'll scale it.

Unrealistic valuation expectations. Seed-to-pre-A step-ups are usually 1.5×–3×. Asking for a 5×+ jump without extraordinary metrics loses credibility.

Ignoring existing investor rights. Seed investors may hold pro-rata or anti-dilution protection. Mishandling those in the pre-A can trigger disputes — talk to them first about whether they're following on.

Raising too late. Ideally you start the pre-A with 9–12 months of runway. At 3–4 months, investors know you're desperate and the terms tighten sharply.

Under-prepared documents. Diligence is lighter than a Series A, but investors will ask for financials, user data, contracts, and the cap table. Scrambling when asked signals weak operational control.

Frequently Asked Questions

What's the difference between a pre-A round and a bridge round? They're structurally similar but positioned differently. A bridge is usually a small, short-term top-up (often a convertible note or SAFE) taken after you already have preliminary Series A interest, to reach closing. A pre-A is a standalone round with its own term sheet, valuation, and investor base. In short: a bridge gets you to closing; a pre-A gets you to the A.

How long does a pre-A take to close? Typically 6–10 weeks from first investor contact to money in the bank — longer than a seed (deeper diligence) but shorter than a Series A (lighter legal work). Roughly: 1–2 weeks of term-sheet negotiation, 2–3 weeks of diligence, and 2–3 weeks of legal documents and signing.

Can I use a SAFE or convertible note for a pre-A? Yes. Many pre-A rounds are done as a SAFE or convertible-note bridge because they close faster and defer valuation. Others use priced preferred equity when the new lead wants defined rights. The choice depends on your investors, your leverage, and how much you want to fix a valuation now versus at the A.

What role do seed investors play in a pre-A? They may follow on (especially if they hold pro-rata rights). Good seed investors also introduce you to pre-A leads, provide reference calls, or even lead the round themselves. Communicate your plan to them before you open the round.

Do I need a lawyer for a pre-A? Strongly recommended. Even though the documents are lighter than a Series A, anti-dilution, preference, and shareholder-agreement amendments have real downstream consequences. Using AI document tools to prepare strong first drafts reduces your counsel's hours — and your bill.

The Bottom Line

A pre-A round is a distinct waypoint on the fundraising journey — not a bigger seed, not a smaller Series A. Investors underwrite PMF signals, repeatable growth, improving unit economics, and a credible path to the A. Prepare the full document package (deck, financial model, cap table, term sheet, investment agreement, data room) before you open the round, start while you still have 9–12 months of runway, and don't ignore your existing investors' rights.

When your term sheet or investment documents arrive, upload them to AiDocX and let AI explain the valuation, dilution, anti-dilution, and board terms in plain English before you sign — free to start.

Ready to automate your documents with AI?

Start free with AiDocX — AI contract drafting, meeting minutes, consultation notes, e-signatures, and more in one platform.

Get Started FreeMore from AiDocX Blog

Anti-Dilution Provisions Explained: What Founders Must Know (2026)

A founder's guide to anti-dilution provisions in investment agreements — how full ratchet and weighted-average protection work, what happens in a down round, and how each option affects your equity. With a worked calculation and ready-to-use clause templates.

Chat With Your Contract: How to Ask AI Questions About Any Document (2026)

Learn how to chat with a contract using AI — ask plain-English questions about clauses, deadlines, and risks instead of reading 30 pages. How it works, what to ask, and why a purpose-built tool beats pasting into ChatGPT.

Employee Stock Option Plans (ESOP) for Startups: Vesting, Pools, and Templates (2026)

A founder's guide to employee stock option plans — how options and vesting work, how big your option pool should be, the documents you need, and the mistakes that cost startups equity. With a free template workflow.